TSMC, five other foundries with more than $1.0 billion in revenue.

Information in this Research Bulletin comes from the 2014 edition of IC Insights’ McClean Report. The 900-page report includes over 400 charts and figures! Details of the new report are provided at the end of this bulletin.

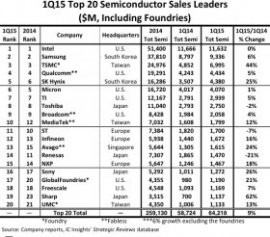

IC Insights’ ranking of the leading IC foundries—both pure-play and IDM—by foundry sales for 2013 is shown in Figure 1. In total, the top 13 foundries in the figure represented 91% of total foundry sales in 2013. For comparison, the leading 13 foundries accounted for 84% of total foundry marketshare in 2009, the year before Samsung dramatically ramped up its IC foundry production for Apple.

Figure 1

TSMC, by far, remained the leader with almost $20 billion in sales in 2013. In fact, TSMC’s 2013 sales were over 4x that of second-ranked GlobalFoundries and 10x the sales of the fifth-ranked foundry SMIC. As shown, there are only three IDM foundries in the ranking—Samsung, IBM, and MagnaChip. Samsung was easily the largest IDM foundry in 2013 with over 8x the sales of IBM, the second-largest IDM foundry.

Powerchip has recently done very well in the foundry business after struggling to remain competitive in the DRAM business. Powerchip announced in January 2011 that it would stop selling DRAMs under its own brand name to focus on producing other devices such as LCD drivers, CMOS image sensors, flash memory, and power management devices both for self-branded products and on a foundry basis for others. The move came after Powerchip agreed to sell all of its DRAM-production output to Elpida, which had been buying about half of the company's commodity DRAMs under a previous foundry agreement.

In 2011, Powerchip’s foundry sales were $374 million, which represented 29% of the company’s semiconductor sales. In 2012, Powerchip’s foundry sales surged 67% to $625 million, which represented 67% of the company’s total semiconductor sales, and in 2013, Powerchip’s disclosed that it had made the complete transition to a pure-play foundry with sales reaching $1, 175 million, 100% of the company’s total IC sales. Slowly but surely the company has transformed itself into a major IC foundry.

In 2013, Samsung had a 15% increase in its foundry sales and was less than $10 million behind the third-largest IC foundry in the world—UMC. Samsung has the ability (i.e., leading-edge capacity and a huge capital spending budget) and desire to become a major force in the IC foundry business. It is estimated that the company’s dedicated IC foundry capacity reached 150K 300mm wafers per month in 4Q13. Using an average-revenue-per-wafer figure of $3, 000, it is estimated that Samsung’s IC foundry business segment has the potential to produce annual sales of about $5.4 billion.

RELATED VIDEO

RELATED FACTS

-

A foundry is a factory that produces metal castings. Metals are cast into shapes by melting them into a liquid, pouring the metal in a mold, and removing the mold material or casting after the metal has solidified as it cools. The most common metals processed are...

A foundry is a factory that produces metal castings. Metals are cast into shapes by melting them into a liquid, pouring the metal in a mold, and removing the mold material or casting after the metal has solidified as it cools. The most common metals processed are...

-

Buehler-Garcia brings to Ponte a lengthy track record in high-tech

dating to the early 1980s.

Before joining Ponte, he was managing director for Alanza Technologies,

a consulting company to the semiconductor ecosystem. Buehler-Garcia previously held the... - Fluorosilicate glass (FSG) is a low-k dielectric used in between copper metal layers during silicon integrated circuit fabrication process. It has a low dielectric constant (k) and is now widely adopted by semiconductor foundries on geometries sub 0.25�...

Share this Post

latest post

-

Semiconductor Processing November 26, 2023

Semiconductor Processing November 26, 2023 -

Top Fabless Semiconductor companies October 27, 2023

Top Fabless Semiconductor companies October 27, 2023 -

Silicon Valley Semiconductor companies September 27, 2023

Silicon Valley Semiconductor companies September 27, 2023 -

New Semiconductor companies August 28, 2023

New Semiconductor companies August 28, 2023 -

List of Semiconductor companies in USA July 29, 2023

List of Semiconductor companies in USA July 29, 2023 -

Semiconductor properties June 29, 2023

Semiconductor properties June 29, 2023 -

Semiconductor industry companies May 30, 2023

Semiconductor industry companies May 30, 2023 -

Canadian Semiconductor company April 30, 2023

Canadian Semiconductor company April 30, 2023 -

Semiconductor companies in Europe March 31, 2023

Semiconductor companies in Europe March 31, 2023 -

Semiconductor jobs in Europe March 1, 2023

Semiconductor jobs in Europe March 1, 2023 -

Freescale Semiconductor, Ltd January 30, 2023

Freescale Semiconductor, Ltd January 30, 2023 -

Freescale Semiconductor Patent December 31, 2022

Freescale Semiconductor Patent December 31, 2022 -

Freescale Semiconductor news December 1, 2022

Freescale Semiconductor news December 1, 2022 -

Freescale Semiconductor stock symbol November 1, 2022

Freescale Semiconductor stock symbol November 1, 2022 -

Global Semiconductor company October 28, 2022

Global Semiconductor company October 28, 2022